Financial well-being of workers dives as costs soar, National Payroll Institute survey says

Reviews and recommendations are unbiased and products are independently selected. Postmedia may earn an affiliate commission from purchases made through links on this page.

Article content

Good morning!

Advertisement 2

Article content

Article content

More employed Canadians are finding themselves on shaky financial ground as inflation and higher interest rates erode any savings gains they made during pandemic lockdowns — and the worst may be yet to come.

The financial well-being of workers has fallen sharply this year amid rising expenses brought on by soaring living costs, according to the annual survey of working Canadians from the National Payroll Institute. More people say they’re finding it difficult to stretch their income to cover their bills, with the number of those living paycheque-to-paycheque jumping 26 per cent compared to this time last year.

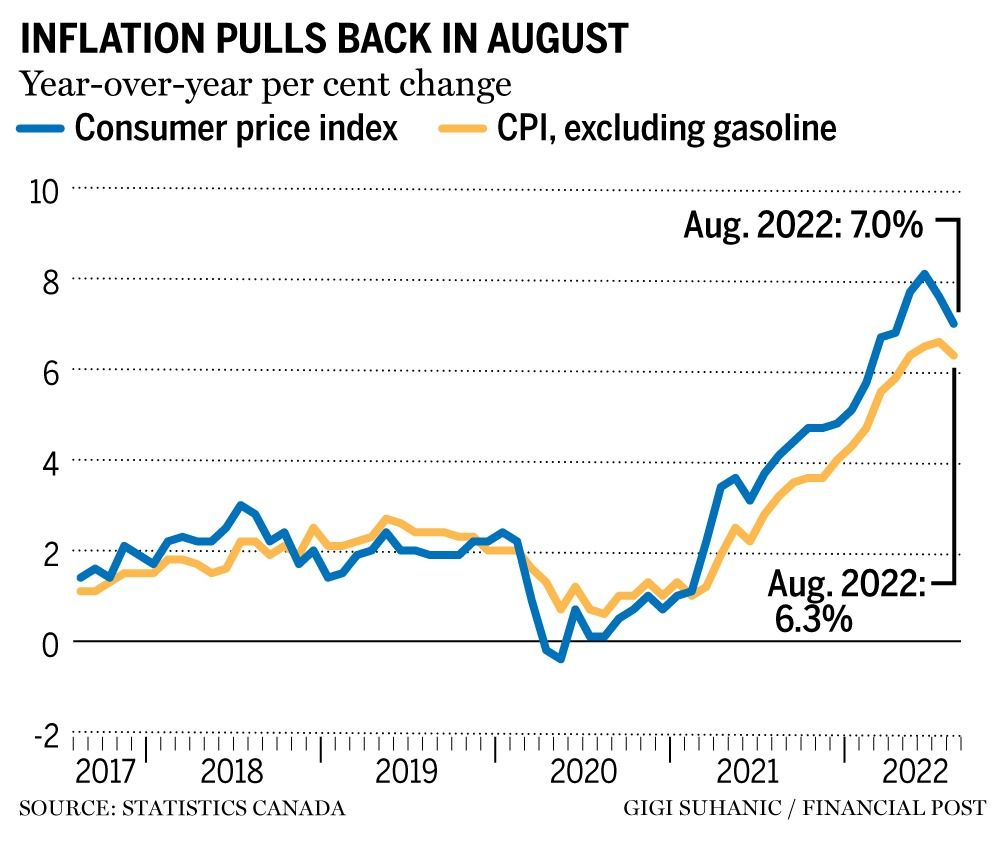

The days of solely working from home, saving on commuting costs and socking away money in savings accounts are behind most Canadians. Budgets are now getting stretched as more people head back to the office amid higher debt costs from rising interest rates and inflation hovering at levels not seen since the 1980s. Though the consumer price index has decelerated for the past two months, it still remains high. CPI clocked in at seven per cent in August, Statistics Canada said yesterday. Gas prices are cooling but food prices continue to rise, and were up 10.8 per cent from a year ago, putting pressure on wallets.

Advertisement 3

Article content

To get by, people are piling on debt. Those spending more than they make climbed 11 per cent — the highest ever in the survey’s history. Meanwhile, the number of workers carrying credit card debt soared to 42 per cent, climbing from 29 per cent in 2021, the survey said.

Savings are getting neglected, too. Nine per cent of workers say they don’t save at all, while 34 per cent say they put aside only one to five per cent of their paychecks, up from 27 per cent last year, when people reported being more financially stable.

There are other signs that workers are struggling under the burden of higher costs. One way the institute measures financial health is by placing people into three categories, or “clusters”: those who are comfortable, those who are coping, and those who are stressed. Last year, 46 per cent of respondents said they were comfortable financially. But this year, eight per cent of those joined the coping category, and another two per cent went over to the stressed section.

Advertisement 4

Article content

And it’s not over yet. The “financial stress storm” is just getting started, the institute said.

“The data indicates that things are likely to become even more difficult for people in the near future,” Peter Tzanetakis, president of the National Payroll Institute, said in a news release.

“Savings and spending habits, along with reliance on debt, have consistently determined the cluster an individual belongs to, and each one is moving in the wrong direction. With rising interest rates and inflation still an issue, it is likely that this trend will continue,” he said.

Heightened financial stress isn’t just limited to those who have lower incomes, either. According to the survey, 41 per cent of households who said they are stressed financially make $100,000 or more annually.

Advertisement 5

Article content

To cope with rising food costs, many are using debt to buy groceries and other essentials. They’re also changing their shopping habits. A separate survey from the Agri-Food Analytics Lab at Dalhousie University, in partnership with Caddle, found that close to three out of four Canadians are getting creative with how they buy groceries. They are making using of loyalty programs to pay for groceries, scanning flyers, using coupons and visiting discount stores to trim their bills.

That’s a step in the right direction. According to the National Payroll Institute’s survey, many people dealing with financial anxiety tend to throw in the towel because they aren’t sure how to find relief. But, “doing nothing will not help them weather the storm,” the institute said.

Advertisement 6

Article content

The group says the first step out of financial distress is to take stock of your budget, and then act immediately to take control.

“The storm will likely not last forever, but the sooner you take action to build stronger financial habits, the brighter the forecast ahead,” the institute said.

__________________________________________________________________________

Was this newsletter forwarded to you? Sign up here to get it delivered to your inbox.

__________________________________________________________________________

LUMBER BELLWETHER Lumber prices shot up early in the pandemic, it proved to be a signal that inflation was rising. But if the lumber was an early indicator of where prices are headed, then the central bankers who are now trying to beat back the hottest inflation since the 1980s may take heart in recent signals coming from the lumber market. A growing number of Canada’s largest producers, including Canfor Corp. and West Fraser Timber Co. Ltd., recently announced plans to scale back production in British Columbia, citing softening demand among other factors, writes the Financial Post’s Gabriel Friedman. Analysts believe that softening demand could be a sign that interest rates are doing their work, cooling demand and tamping back inflation. Photo by James MacDonald/Bloomberg

Advertisement 7

Article content

___________________________________________________

- Statistics Canada releases “Canada’s housing portrait”

- US House Financial Services Committee hearing “Holding Megabanks Accountable: Oversight of America’s Largest Consumer Facing Banks”

- US Federal Reserve releases interest rate decision and updated forecasts, with a news conference from chair Jerome Powell to follow

- Gord Nelson, Cineplex chief financial officer, will speak at the 21st annual CIBC Eastern Institutional Investor conference

- Charlie Angus, NDP natural resources, jobs and just transition critic; and MP for Timmins—James Bay, will lay out the NDP’s plan for Canada’s green job transition and will speak about his party’s priorities this fall session to fight for energy workers, their communities and their families’ future

- The standing committee on finance holds a meeting about the current state of fiscal federalism in Canada

- The standing committee on foreign affairs and international development holds a meeting about the business committee regarding future plans in relation to the study of export of Russian Gazprom turbines

- Alberta Premier Jason Kenney will launch the next phase of the Alberta is Calling campaign that offers skilled workers from across the country a glimpse into the life that awaits them in Alberta

- Alberta Investment Management Corporation (AIMCo), Alberta’s institutional investor managing over 30 public funds and pensions, will host a ribbon-cutting event with CEO Evan Siddall and Calgary Mayor Jyoti Gondek to celebrate the opening of AIMCo’s new Calgary office location

- Environment and Climate Change Minister Steven Guilbeault will participate in the High Ambition Coalition to End Plastic Pollution side-event during the opening of the 77th UN General Assembly

- Prime Minister Justin Trudeau will attend a meeting of the High Level Panel for a Sustainable Ocean Economy entitled “Financing Ocean Solutions for People and Planet: Delivering on SDG 14″

- Mary Ng, minister of international trade, export promotion, small business and economic development, will meet with her G20 counterparts

- Today’s data: Canadian new housing price index; US existing home sales

- Earnings: General Mills Inc.

Advertisement 8

Article content

___________________________________________________

_________________________________________________________

_____________________________________________

Advertisement 9

Article content

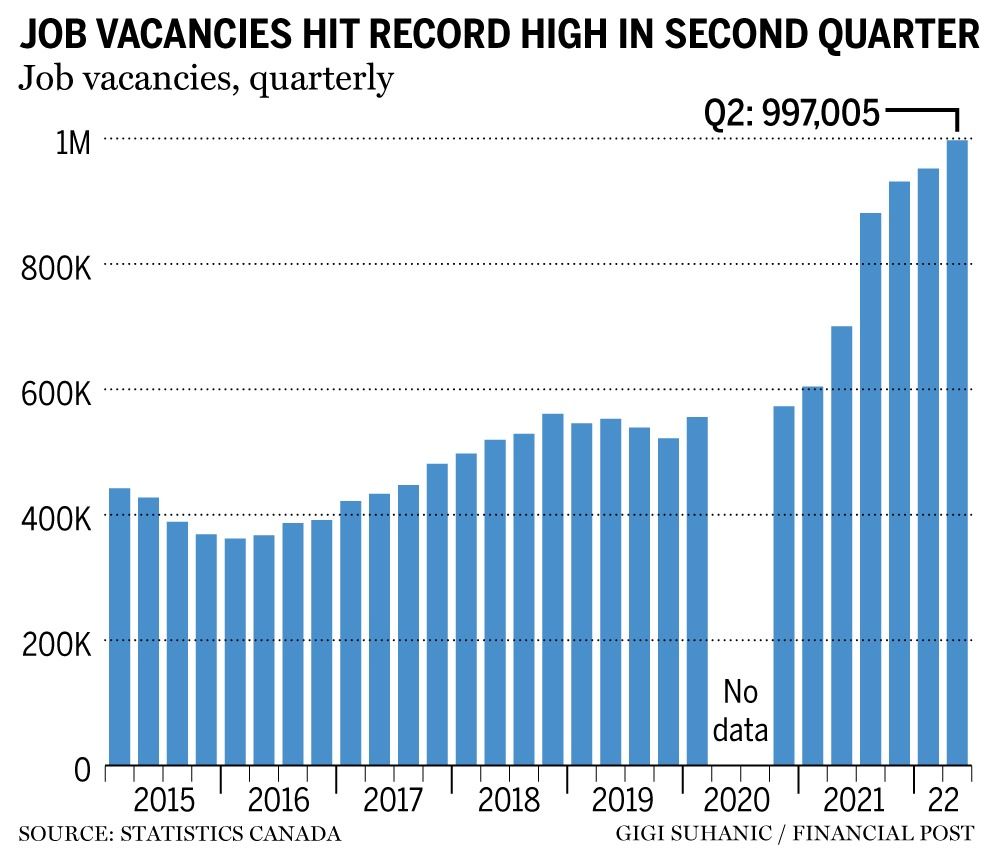

Job vacancies hit a record in the second quarter of 2022, but employers struggled to fill those empty positions still offered wage increases that were lower than the rate of inflation.

Statistics Canada on Sept. 20 said there were nearly one million unfilled positions in the second quarter, the highest quarterly number on record. That’s up by 45,000 vacancies from the prior quarter and is 42.3 per cent higher than in 2021.

The vacancy rate, which measures unfilled positions as a percentage of total labor demand, was 5.7 per cent — also an all-time high.

The overall average hourly wage increased 5.3 per cent to $24.05, compared to a 7.5 per cent increase in the consumer price index (CPI).

______________________________________________

Advertisement 10

Article content

Becoming an executor of a loved one’s estate requires a lot of work and a large time commitment, made more difficult during a period of grieving. Before you agree to the job, it pays to know what to expect first. The Financial Post offers some advice for anyone considering becoming an executor in the latest installation of the Money Milestones series.

______________________________________________

Today’s Posthaste was written by Victoria Wells (@vwells80), with additional reporting from The Canadian Press, Thomson Reuters and Bloomberg.

Have a story idea, pitch, embargoed report, or a suggestion for this newsletter? Email us at [email protected], or hit reply to send us a note.

Listen to Down to Business for in-depth discussions and insights into the latest in Canadian business, available wherever you get your podcasts. Check out the latest episodes below: